Indexed Universal Life Insurance: Upside Potential and Downside Protection

Most people know that life insurance provides a death benefit when you die.

But permanent life insurance also offers the potential to grow the value of your policy. With indexed universal life insurance, this potential cash value growth is based on the performance of a market index (e.g., the S&P® 500).

When you invest in the stock market, you may see impressive gains, but you’re also at risk of losses.

That’s not true for indexed life insurance, which provides downside protection. All National Life Group indexed universal life insurance products offer a zero percent floor — the least interest you are ever credited is 0%.

If you need death benefit protection and are interested in growing the cash value of your policy without market risk, indexed universal life insurance may be worth considering.

Key things to know about the upside potential and downside protection offered by indexed life insurance:

- The potential growth of the cash value of an indexed universal life insurance policy is based on the performance of a market index like the S&P 500 or on a fixed interest rate.

- You typically have a choice of multiple index crediting options.

- Indexed universal life insurance policies aren't directly invested in a market index.

- Caps and participation rates are important factors in determining how much interest is credited when the market goes up.

- Indexed universal life insurance offers protection and a zero percent floor when the market goes down.

What is the upside potential of indexed life insurance?

The potential growth of an indexed universal life insurance policy is based on the performance of a market index in a given period (usually over a one- or two-year period).

A well-known example of a market index is the S&P 500, which includes a representative sample of 500 leading companies in leading industries of the U.S. economy.

Indexed universal life insurance typically offers a choice of interest crediting strategies based on different market indexes, including some that are designed to reduce volatility.

Which index crediting option should I choose?

That is up to you! No one can predict how the market will perform — and just because an index performed a certain way in the past, doesn’t mean it will perform that way in the future. You can also pick more than one index crediting option. However, remember that diversification does not assure a better return.

What if I am worried about having just an annual crediting anniversary?

You have the option to spread your premiums over 12 months, using the Systematic Allocation Rider.

Spreading out your premium over a 12-month period helps capitalize on more potential interest rate crediting dates and reduces risk associated with one annual crediting anniversary. However, this does not guarantee better outcomes.

Until allocated into a monthly crediting strategy, premiums will earn interest in a fixed interest crediting account.

Can I change allocations?

Yes, you can how you allocate money across index crediting options at any time. Your new allocations will take effect at the start of the next crediting period. You can change your allocations using the National Life Group customer portal or via our app.

DOWNLOAD THE CUSTOMER APP

Will my savings grow as much as when I invest directly in the stock market?

Not necessarily. How much interest you are credited depends not just on the performance of the market index, but also on the participation rate and whether there is a cap.

What is a cap?

The cap determines the maximum interest you can earn in a period. For example, if the index grows by 10% but your cap is 6%, your policy will be credited with 6% interest.

Not all index strategies are capped.

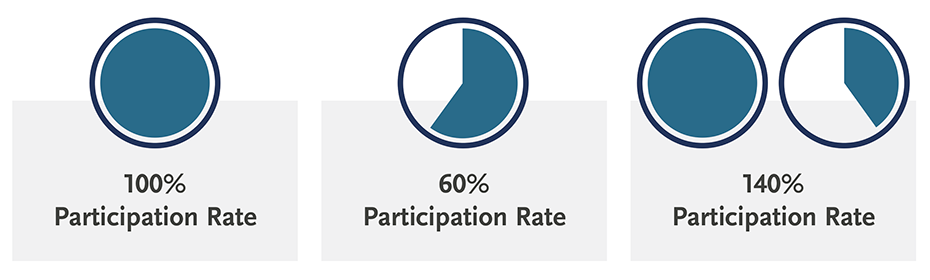

What is the participation rate?

The participation rate determines how much of the market index gains are credited to your policy.

Here are examples illustrating how interest is credited for a specific time period (known as “point to point”), which can be one or two years:

- If the market index gained 8.00% and the participation rate is 140%, you would get credited 11.20% if there is no cap.

- If the market index gained 8.00% and the participation rate is 60%, you would get credited 4.80% if there is no cap.

- The participation rate can also be 100%. In that case, you would get credited at the same rate as the market index gain if there is no cap.

What is the downside protection of indexed life insurance?

Sometimes markets go down and an index may lose value in a given period. If you are invested directly in the index, like when you invest in the stock market, you would lose money during a downturn.

That’s not true for indexed universal life insurance from National Life Group. When a market index goes down, you are protected from loss. All our indexed universal life insurance products offer a zero percent floor — the least interest you are ever credited is 0%.

Next steps?

- View the differences between interest crediting options and historical performance.

- Learn about volatility-controlled indexes.

- Find out what is best for you and your unique situation: Work with your agent or a financial/tax professional.